See market behavior clearly — without the trading paranoia.

Compare plans to track liquidity and structure instead of reacting emotionally.

Trading Basics

May 12, 2026

SHARE

The Trading Boogeyman: Why “They’re Out to Get Me” Keeps Traders Stuck

Every trader has heard statements like, “They stopped me out and then the price moved in my direction,” or “Market makers saw my stop.” Over time, repeated experiences like these can make it seem as if market makers are hunting stops or that prices are intentionally moved against retail positions. This belief further strengthens after a series of frustrating trades, giving rise to common trading conspiracy theories.

However, in most cases, the market is not reacting to any single participant. Instead, price moves are influenced by liquidity, positioning, and trading patterns (created by many traders placing similar orders at similar levels). Thus, what appears as manipulated market trading is just a natural outcome of how markets operate.

This article explains why such beliefs develop, what is actually happening behind so-called “market makers hunting stops”, and shows how traders can shift from blame toward a better view of market behavior.

Why Traders Create a Boogeyman in the First Place

Trading involves strong emotions, and losses usually feel personal. This happens because:

- Money is at stake

- Decisions are “self-directed”

- Outcomes appear immediately, and

- Regret can be intense

As a result, when a stop-loss is triggered and the price reverses soon after, the mind looks for a cause. At this point, many participants begin to believe in ideas such as “market makers hunting stops”. Such beliefs fall under trading conspiracy theories and narratives around manipulated market trading. The explanation appears logical on the surface because the timing of the reversal feels deliberate.

However, this reaction is more due to emotional discomfort than to objective analysis. It is easier to assign blame to “market makers,” institutions, or algorithms than to examine the trade itself. This is why many traders end up asking why traders blame market makers, even when no direct evidence exists. In reality, several mistakes usually lead to such wrong execution:

At times, the outcome is a result of “random probability” rather than deliberate targeting. Realize that conspiracy narratives emerge from a combination of emotional stress and incomplete knowledge of how markets function. Not following a setup is a big cause for this ‘boogeyman’. Improve your trading outcomes by applying for Bookmap’s Pilot Program by Bruce.

No One Is Hunting Your Single Position

Most retail participants assume that an individual trade is large enough to attract direct attention. However, financial markets operate at a scale where thousands of participants interact simultaneously (each with different goals and order sizes). Thus, a small futures position, stock trade, or CFD stop carries little significance in the broader flow of orders.

This also does not mean that stops are not triggered. Instead, it explains why the idea of market makers hunting stops is usually misunderstood. Traders must be aware that price movements are rarely designed to target a single position. Rather, they are driven by the need to match large volumes of buying and selling interest.

Consequently, markets may move toward areas where many orders are concentrated. These areas have the following characteristics:

Such zones are commonly referred to as “liquidity pools,” where a higher number of orders increases the probability of execution. This behavior is often misinterpreted as market makers hunting stops. In reality, it reflects market mechanics rather than intent. The movement is not personal; it is a function of how liquidity is distributed across price levels.

Therefore, what appears to be manipulated is a result of “collective positioning”. Realize that the market does not need access to any single order. Instead, it reacts to patterns created by many participants placing trades in similar locations.

What Traders Call “Stop Hunts” Are Usually Liquidity Events

One of the most common reactions in trading is the belief that “they ran my stop.” This perception usually appears when the price moves beyond a visible level, such as a:

- Prior high

- Price low

- Support or resistance level, or

- Trend line

Next, such price movement triggers stop losses and then reverses sharply. As a result, the move feels intentional and feeds into ideas like market makers hunting stops. However, this behavior is more accurately explained by how markets search for liquidity.

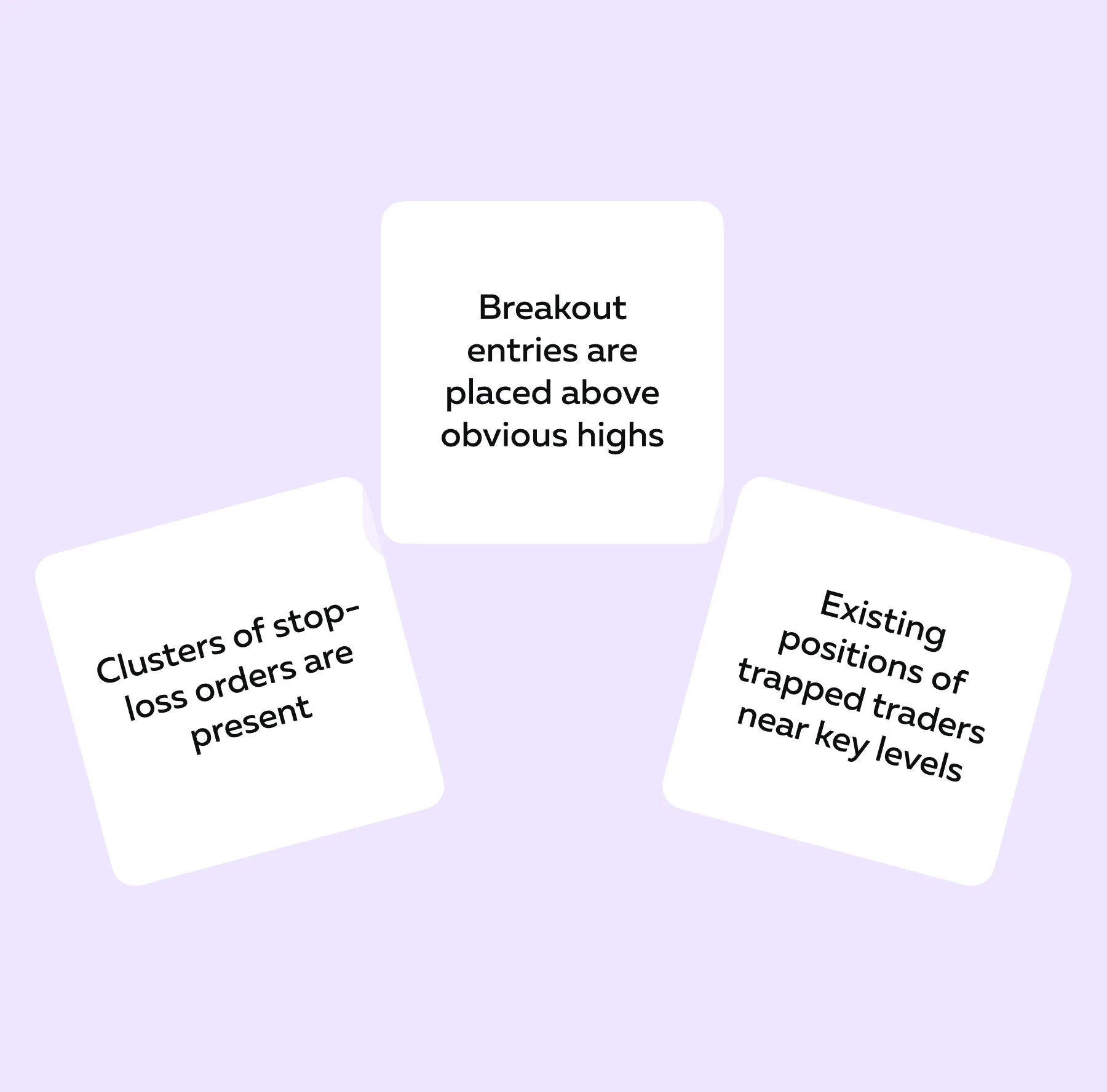

Realize that markets require active buyers and sellers to complete transactions, and this activity mostly concentrates around obvious technical levels. These areas naturally attract a high number of orders, which creates dense pockets of liquidity.

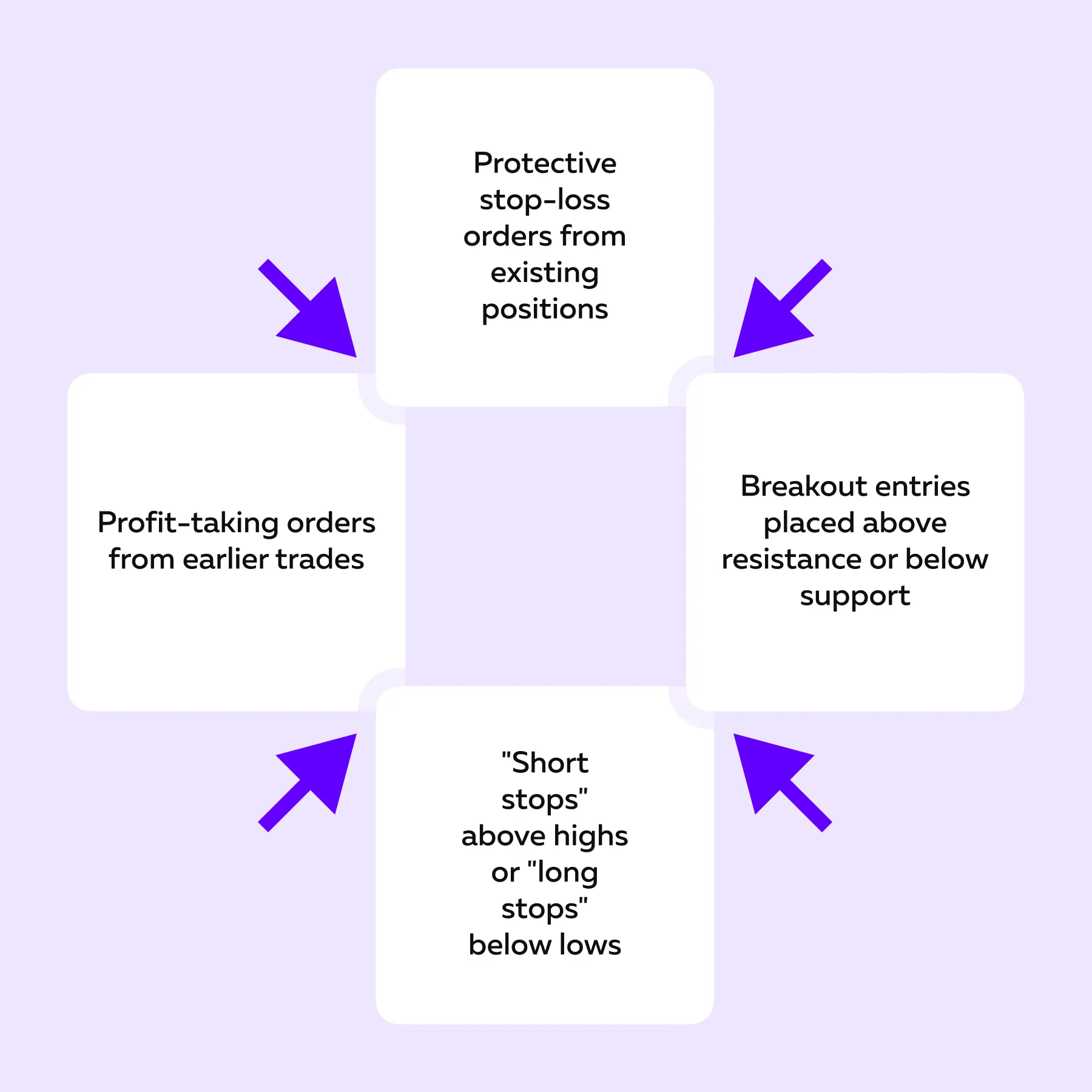

These liquidity zones may contain the following:

As a result, when the price approaches such a level, it is not targeting individuals but interacting with a large cluster of orders. Let’s understand better through an illustrative example:

| Stage | Market Behavior |

| Setup | Price trades below resistance at 4500 for an extended period. |

| Order Build-up | Traders place:

|

| Trigger | Price moves to 4502, activating stops and breakout orders. |

| Reaction | Buying volume increases sharply due to triggered orders. |

| Outcome | Passive sellers absorb this demand. Later, once buying weakens, the price rotates lower. |

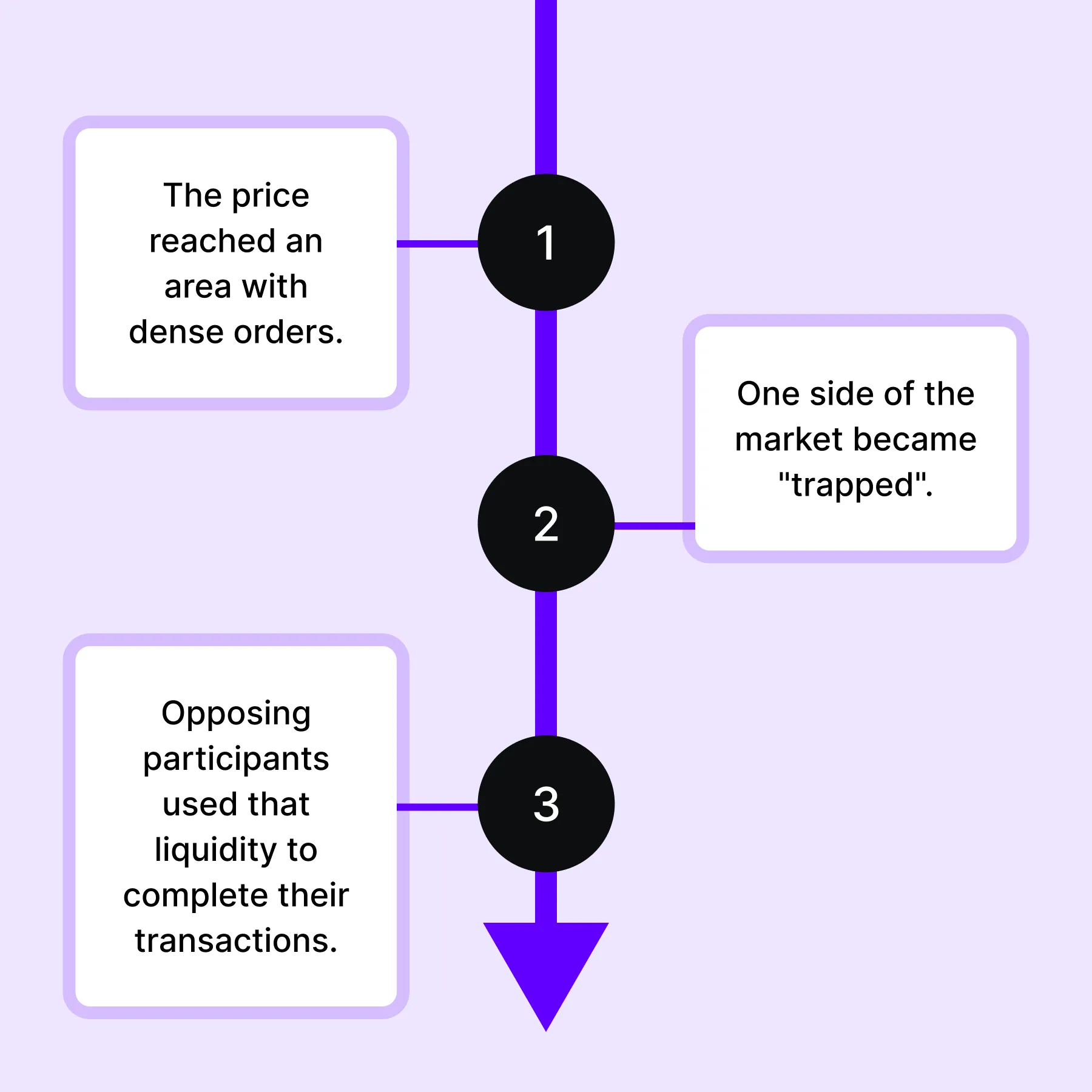

Usually, this sequence appears as “manipulated” to those affected by the reversal. However, the move only reflects this sequence:

- Price enters a high-liquidity zone

- Trades get executed

- Price is adjusted once the order flow is absorbed

Therefore, what is commonly described as “stop hunts” does not automatically indicate predatory intent. Instead, it usually signals that:

Understand liquidity instead of blaming manipulation → Compare Packages

What Market Makers Actually Do (And Why They Get Blamed)

Many participants use the term “market makers” as a broad explanation for unfavorable outcomes. However, this view usually comes from limited clarity about their actual role. In reality, market makers operate to support trading activity as follows:

As market conditions change, particularly during periods of higher volatility, they also adjust positions to reduce risk. As a result, their behavior can sometimes appear frustrating. For example,

- Liquidity may be reduced ahead of a sharp move, or

- New liquidity may appear near resistance levels

Additionally, in uncertain conditions, spreads may widen, and after large order flow, hedging activity may increase. These actions can create price movements that seem unfavorable to many traders.

Consequently, such behavior is often interpreted as market makers hunting stops or evidence of manipulated markets trading. However, from a market structure perspective, these actions are “forms of risk management” rather than targeted intent.

Therefore, uncomfortable price behavior should not be treated as proof of trading conspiracy theories, but rather as a natural outcome of how liquidity providers operate. See what is actually happening behind price movement → Compare Packages

Why Conspiracy Thinking Feels So Real

Despite this, trading conspiracy theories continues to persist because of how human memory processes trading experiences. Painful outcomes may leave a stronger impression than neutral or positive ones.

As a result, traders often remember specific events, and some other outcomes receive less attention. Let’s check them out:

| Painful Events Traders Remember | Events/ Outcomes That Receive Less Attention |

|

|

This imbalance in memory creates a distorted narrative. Over time, repeated exposure to frustrating moments leads to the belief that such outcomes happen consistently and intentionally. Consequently, many begin to blame market makers. However, this perception is influenced by emotional recall rather than objective evidence. Learn how markets move in real time → Compare Packages

How Better Traders Replace Blame With Better Questions

Conspiracy thinking removes a sense of responsibility. When outcomes are attributed to ideas like market makers are hunting stops, the situation appears beyond control. As a result, there is little incentive to review or improve decision-making.

In contrast, more experienced participants shift attention away from blame and toward analysis. Instead of asking why a stop was targeted, they examine how the trade was set up within the broader market context.

This change leads to more constructive questions, such as:

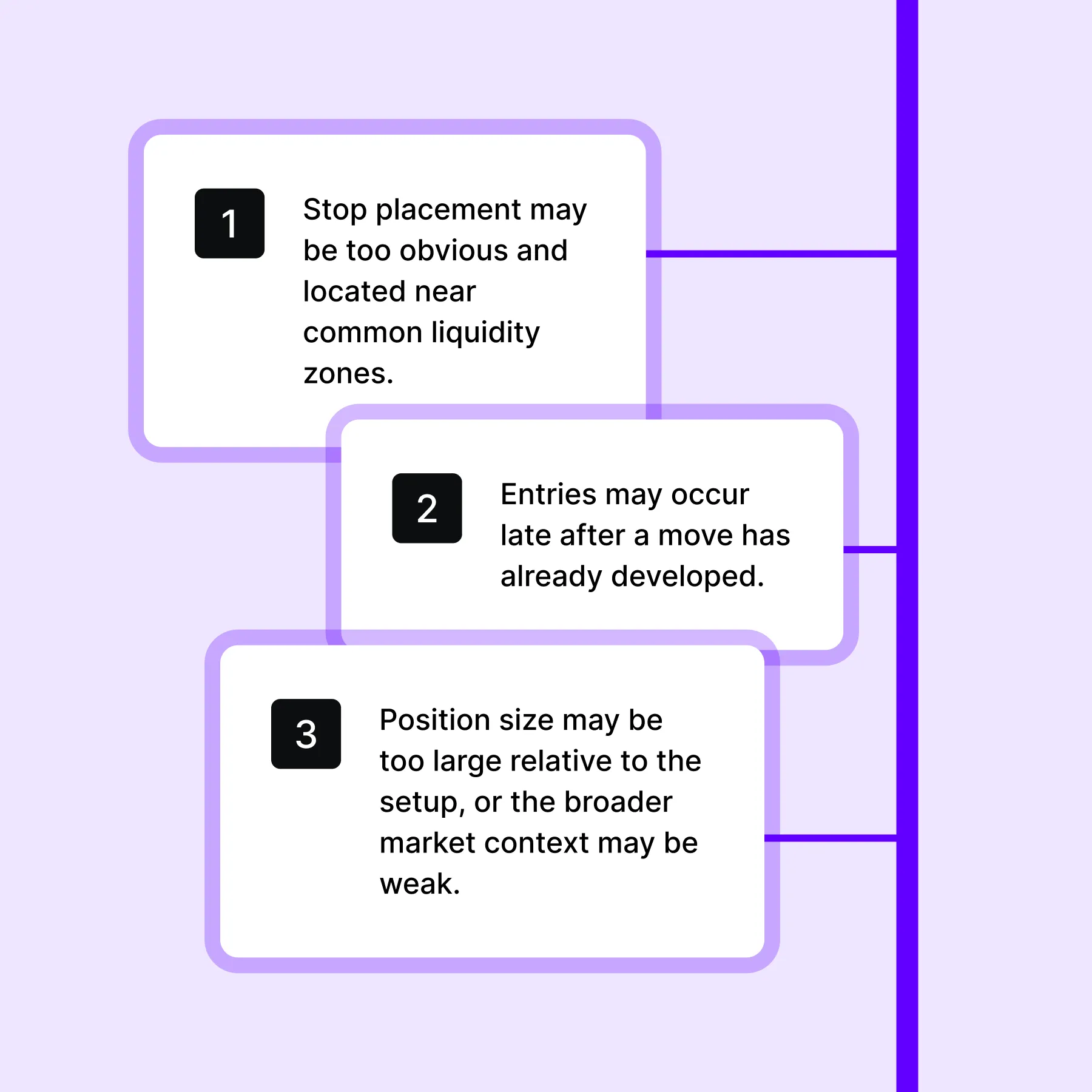

- Whether the stop was placed near an obvious liquidity pool

- Whether the entry occurred late after an extended price move

- Whether the price was in a balanced range where false breakouts are common

- Whether opposing liquidity was present near the intended target

- Whether position size influenced emotional decision-making

- Whether the trade was based on clear confirmation or only expectation

These questions connect directly to observable market behavior. As a result, they provide insight into how price interacts with liquidity, rather than reinforcing beliefs around manipulated markets, trading, or other trading conspiracy theories.

Conclusion

The market is not a villain targeting individual trades or accounts. Instead, it functions as a “competitive auction” where participants seek execution, manage risk, and respond to available liquidity.

At times, price movements may feel unfair or frustrating (particularly when stops are triggered before reversals). However, this does not confirm ideas like market makers stop hunting or other trading conspiracy theories. In many cases, such moves are simply a result of liquidity changes and collective positioning.

Therefore, progress in trading often comes from moving beyond the question of why traders blame market makers and examining actual market behavior. Learn how markets move in real time → Compare Packages

FAQs

1. Do market makers hunt retail stops?

In most cases, no. Individual trades are too small to matter. What may look like market makers hunting stops is actually price moving toward areas where many orders sit together. These clusters create liquidity, which attracts participation.

2. Why does the price reverse after hitting my stop?

As per market understanding, price usually reaches levels where many stops and entries are placed. Once these orders are triggered, a surge in activity occurs. After that, if no strong demand or supply remains, the price can move in the opposite direction. This is commonly interpreted as a “liquidity-driven move” and is not a targeted action.

3. Are markets manipulated?

Some unfair practices can exist, but most price movements are not deliberate manipulation. Many situations described as manipulated market trading are better explained by how liquidity, positioning, and volatility interact. As a result, several trading conspiracy theories arise from misreading normal market behavior.

4. How do I stop feeling like the market is against me?

This feeling mostly comes from repeated frustrating outcomes. Traders may start to see improvements by:

- Reviewing trades

- Analyzing the accuracy of their market timing, and

- Checking their understanding of context

Instead of asking why traders blame market makers, such an approach may shift attention to what the market was doing.

Sign Up Now