See vwap more clearly in real time.

Compare plans to access deeper market visibility for vwap.

Trading Basics

February 12, 2026

SHARE

TWAP vs VWAP: What Traders Need to Know and When Each Matters

At first glance, both TWAP and VWAP appear to be simple averages. Many traders treat them the same and expect similar reactions + signals. But that’s the wrong approach!

Why? That’s because markets don’t trade evenly. And price does not move solely because of time. It moves because of participation, liquidity, and intent. When these factors are ignored, averages lose their meaning, and traders start reacting to levels that were never designed to explain market behavior.

This is precisely where the confusion around TWAP vs VWAP begins. One tool is built to understand where real trading happens. The other exists to control how orders are executed without disturbing the market. They solve very different problems. Want to learn what these averages are? In this article, you’ll learn what each tool truly measures, how institutions use them, and why active traders prefer VWAP.

What VWAP Measures

VWAP stands for Volume Weighted Average Price. It tells you the “average price” at which most trading actually happened during a session (after considering how much volume traded at each price).

VWAP differs from a simple average, which treats every price equally. Instead, it gives more importance to prices where higher volume occurred. So, it reflects where the market truly agreed on value (not just where price briefly moved).

How VWAP Is Calculated and What It Shows

VWAP weights price by volume, not by time, which means:

- A price level where large trades happen will influence VWAP more.

- Small trades or low-volume prices will have a lesser impact.

Additionally, VWAP usually resets at the start of each trading session in intraday charts. Thus, it represents the average transaction price of the day. But what does it tell traders? It answers this question:

- At what price did most participants actually do business today?

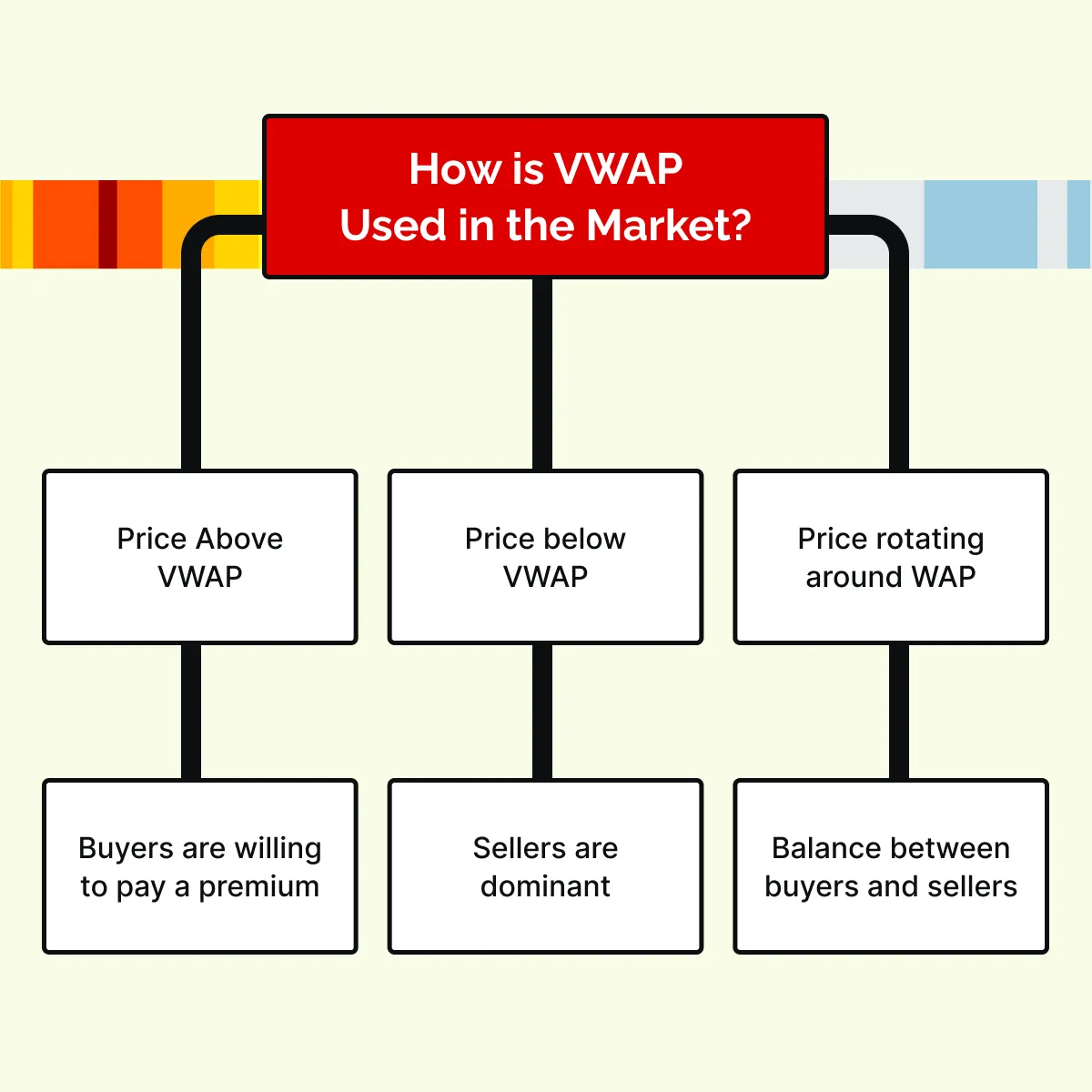

How Important is VWAP For Traders and Institutions?

VWAP is widely used as an “execution benchmark,” especially by institutions. Many large players try to buy below VWAP or sell above VWAP, as that indicates better-than-average execution. Let’s see how market participants use VWAP:

This is why VWAP is often described as a “consensus price”. It shows where participation is concentrated (not where price passes through).

How to Use VWAP in Trading?

VWAP becomes particularly useful after a strong directional move. Once price decisively moves away from a prior area of acceptance, VWAP acts more like a reference point for pullbacks.

Let’s see what many traders do:

- Anchor VWAP to the origin of a major move.

- Wait for pullbacks toward VWAP. Why? They are trying to search for lower-risk re-entry points.

- Avoid chasing prices far from where most transactions occurred.

This is also why scaling or averaging into positions around VWAP can make sense. Instead of entering at a single price, traders let the market rotate back toward a known participation zone.

Remember That VWAP Does Not Predict the Future

VWAP only provides a transaction-based reference. It is just a way to understand where genuine trading interest has already taken place.

What TWAP Measures

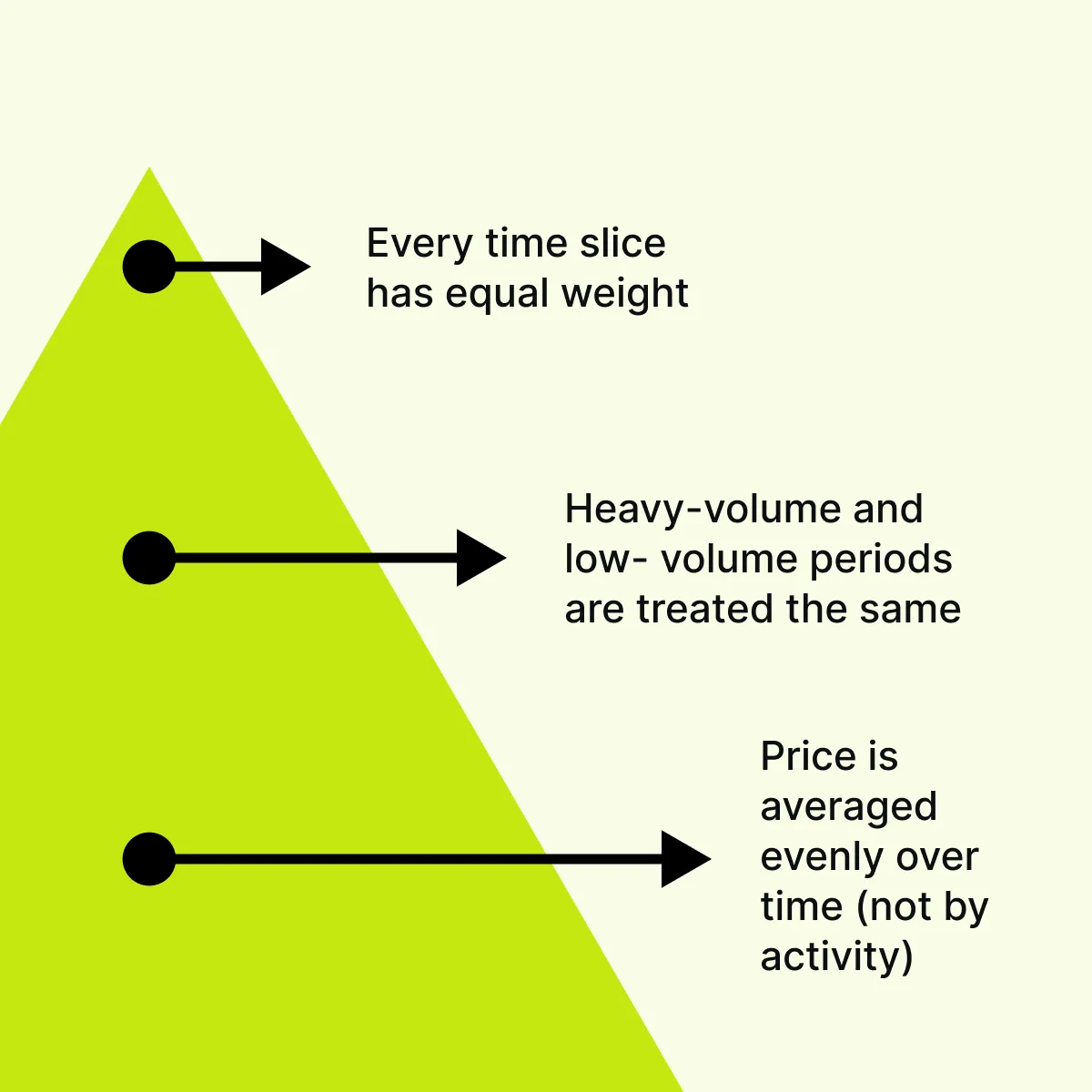

TWAP stands for Time Weighted Average Price. It shows the average price of an asset over a fixed period. In this calculation, each time interval is weighted equally, irrespective of how much volume is traded. Note that TWAP cares about time (not participation).

How TWAP Works: Time Over Volume

TWAP ignores volume completely. It divides a chosen time window, such as market open to close, into equal parts and then averages the price across those intervals. For more clarity, let’s have a look at some of its key characteristics:

It is worth mentioning that TWAP is commonly used “inside execution algorithms”. Usually, it is not considered a trading or market analysis indicator.

Why TWAP Exists and When It Is Used

TWAP was designed to help large traders and institutions execute big orders without moving the market too much. Its main goals are to:

- Reduce market impact,

- Avoid signaling large buying or selling interest, and

- Maintain predictable execution.

Note that TWAP prioritizes discipline and consistency. It is not concerned with “price optimization”. Also, it does not try to get the “best” price. Instead, it only tries to avoid disrupting the market.

Let’s See an Example

Let’s say an institution needs to buy a large quantity of shares during the trading day. Now, the institution does not react to:

- Volume spikes,

- Sudden price moves, and

- Changes in liquidity.

Instead, the order is broken into equal-sized pieces and executed at regular time intervals, from market open to market close. But why? Let’s see some benefits of this approach:

- It keeps execution steady and low-profile,

- It minimizes sudden price jumps caused by large orders, and

- It ignores whether the market is active or quiet at that moment.

In this way, TWAP does not respond to volatility, liquidity, or participation. It simply follows the clock.

How to Think About TWAP

TWAP should be viewed as an “execution scheduling tool”. It must not be used as a tool for understanding market behavior.

Instead, it enforces structured execution over time. This is why, in discussions around TWAP vs VWAP,

- TWAP is about predictability,

and

- VWAP is about where real trading activity happened.

TWAP vs VWAP: The Core Conceptual Difference

Want one of the easiest ways to understand TWAP vs VWAP? Understand this:

| VWAP is “Participation-Aware” | TWAP is “Participation-Agnostic” |

|

|

Why must you understand this difference? Realize that markets do not trade evenly throughout the day. Volume usually clusters:

- Near the market open

- Near the market close, and

- Around news, events, or breakouts.

Now, VWAP adjusts naturally to these volume clusters. TWAP ignores them! It’s important to note that neither tool is “better”. They just answer different questions:

| VWAP Answers | TWAP Answers |

|

|

Connect execution logic with live market behavior → Compare Packages

How Institutions Use VWAP

Institutions commonly use VWAP as a benchmark for execution quality.

From a market behavior perspective, VWAP typically serves as a reference point for liquidity. Why? That’s because during balanced or range-bound sessions, the price frequently rotates around VWAP. Also, traders watch how the price behaves near VWAP to judge acceptance or rejection.

As a result, VWAP can act as an intraday gravity zone. Price may move away during momentum phases, but revisits VWAP when activity slows or balance returns.

How Institutions Use TWAP

Now, TWAP is used very differently. It is primarily an execution scheduling tool and is not used as a market reference. Let’s check out some key situations where institutions use TWAP:

- Executing large orders,

- Trading in thin or illiquid markets, and

- When signaling, the risk needs to be minimized.

Always remember that TWAP is not designed to react to real-time changes in volume, volatility, or liquidity. It follows a fixed plan.

For More Clarity, Let’s Study an Example:

Assume that an algorithm is instructed to execute equal-sized orders:

- At regular intervals

- Over a fixed time window.

Now, the algorithm does this regardless of market conditions. Whether volume spikes or dries up, TWAP keeps executing on schedule. Is there any benefit to this approach? Yes, it:

- Avoids sudden price impact, and

- Does not reveal trading intent to the market.

Why VWAP Is More Useful for Active Traders

VWAP is especially valuable for active and day traders. Reason? That’s because it reflects real market participation. It is:

- Built from actual transactions, and

- Weighted by volume.

Thus, it adapts naturally to how traders are behaving during the session. Understand that active traders benefit from tools that respond to behavior rather than time alone. Want to know how VWAP helps in practice? Let’s check out three core areas where using it proves beneficial:

| Intraday Bias | Context | Extension Analysis |

|

or

|

|

Additionally, there is also a strong connection between VWAP and order flow. That’s because VWAP usually interacts with:

- Liquidity levels,

- Absorption by larger players, and

- Delta and transaction intensity.

Now, all these interactions are visible on the chart, which makes VWAP a preferred tool for real-time decision-making. This is a major reason why, in the discussion of TWAP vs VWAP, active traders rely more on VWAP.

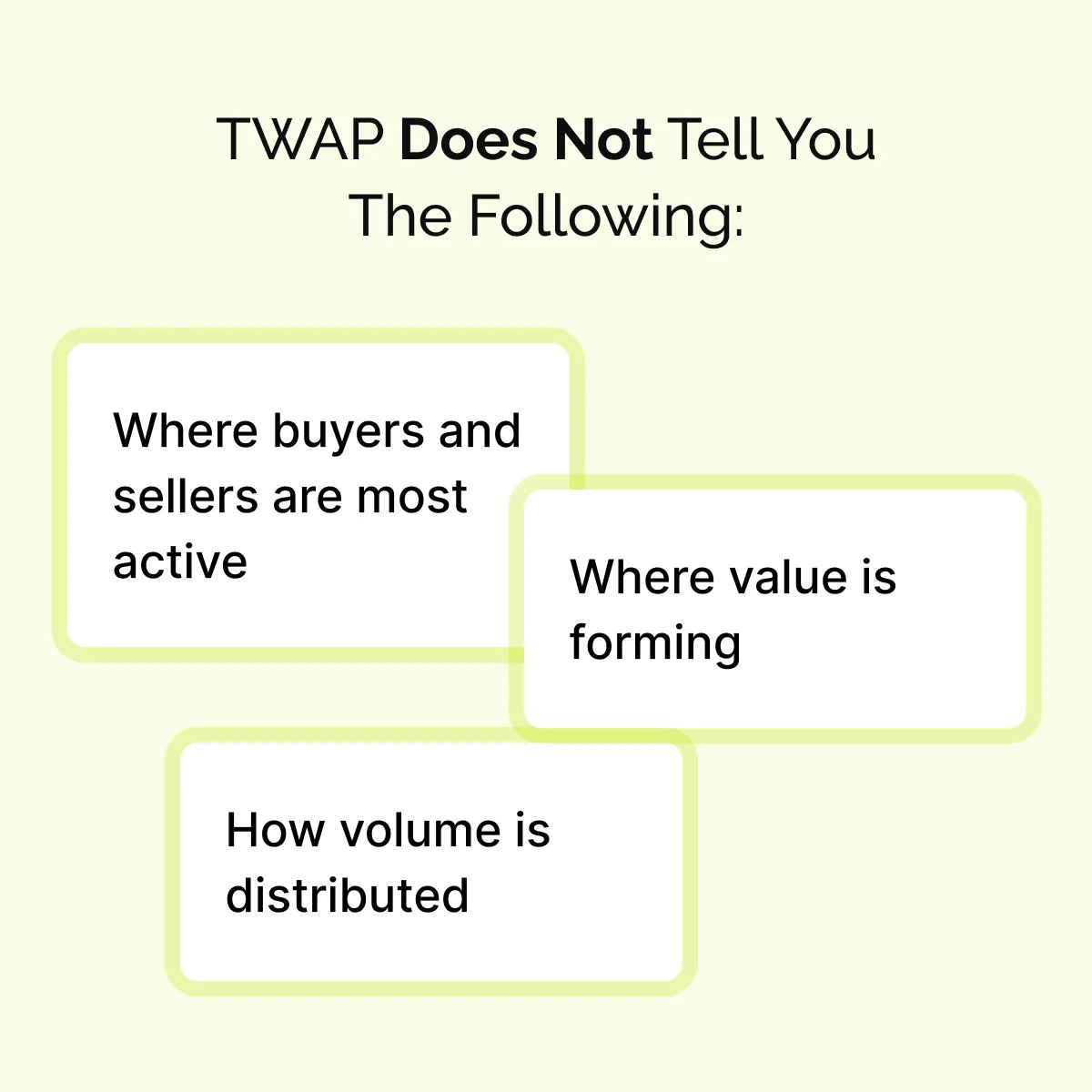

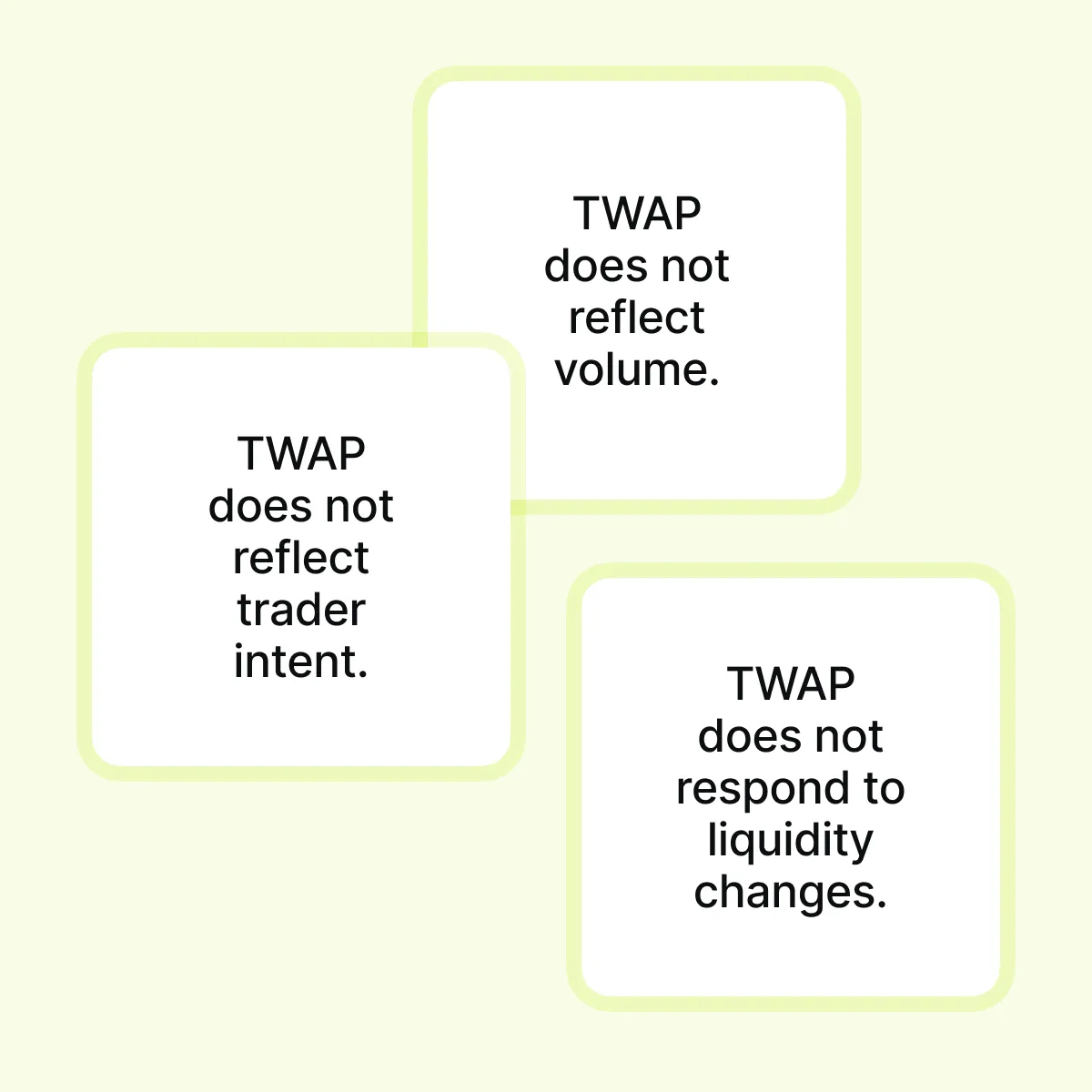

Why TWAP Is Often Misapplied by Retail Traders

TWAP is frequently misunderstood and misused by retail traders. Many treat it as support or resistance and expect the price to react to it. This approach usually does not work. Why? Let’s have a look at some more TWAP limitations:

Also, TWAP is blind to where activity is actually happening. It does not adapt when volume spikes, when liquidity disappears, or when large players step in.

Reading VWAP Through Order Flow

Realize that order flow adds valuable context when price interacts with VWAP. Usually, traders observe the following:

- Do transactions increase or dry up near VWAP?

- Does liquidity rebuild, or does it pull away?

- Does price slow down or accelerate after touching VWAP?

For more clarity, let’s see how traders use VWAP along with order flow in the market:

This behavior-based insight is why VWAP plays such a central role for active traders. Understand where VWAP matters using real-time order flow → Compare Plans.

Using TWAP and VWAP in Trade Planning

In trade planning, the roles of VWAP and TWAP are very different. Let’s see how:

| VWAP Is A Context Tool | TWAP Is An Execution Tool |

|

|

To better understand the concept, let’s now study an example of using VWAP and real-time order flow.

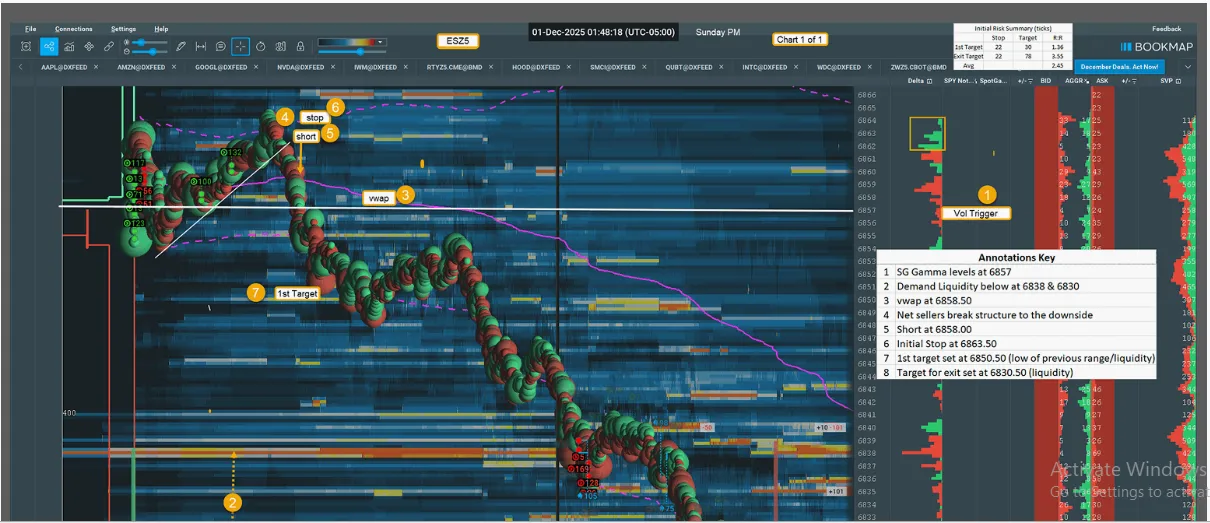

Example: VWAP in Action Using Real Order Flow

The above image is of a real Bookmap chart. It shows:

- How VWAP works in live market conditions, and

- Why VWAP is more useful than TWAP for active traders.

Let’s understand how traders actually make decisions around VWAP using order flow.

VWAP Is a Decision Area, Not Just a Line

In the above chart, VWAP is not treated as a buy-or-sell signal by itself. Instead, it acts as a reference level. It is a place where real participation, liquidity, and execution decisions cluster. Also, the trader does not jump in immediately when the price touches VWAP. Instead, they wait patiently for:

- Price to retest VWAP, and

- Order flow to confirm behavior around that level.

This patience is critical. VWAP tells you where to pay attention and not what to do instantly.

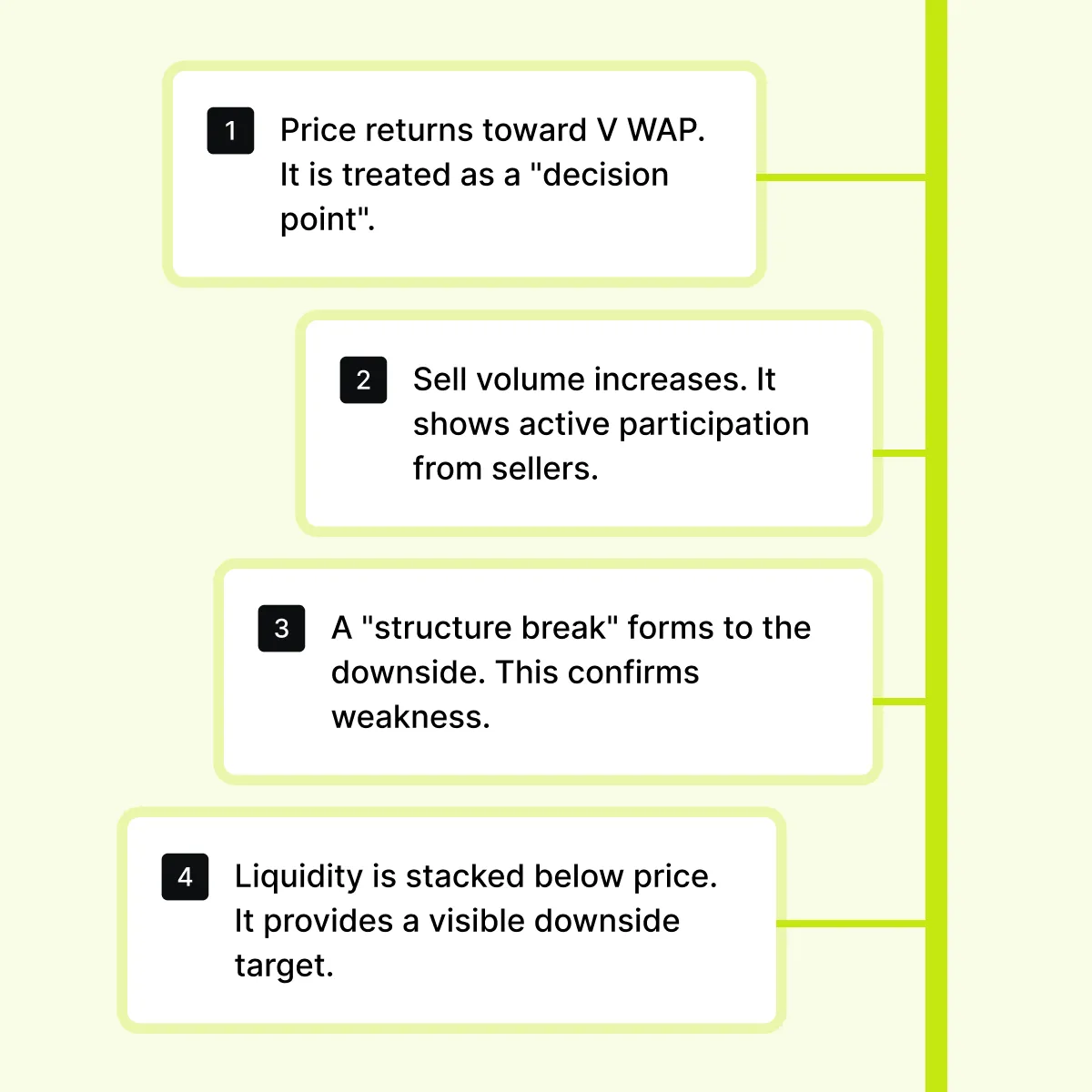

What the Chart Shows Step by Step

Confused with the chart? Let’s see what is happening on the chart step-wise:

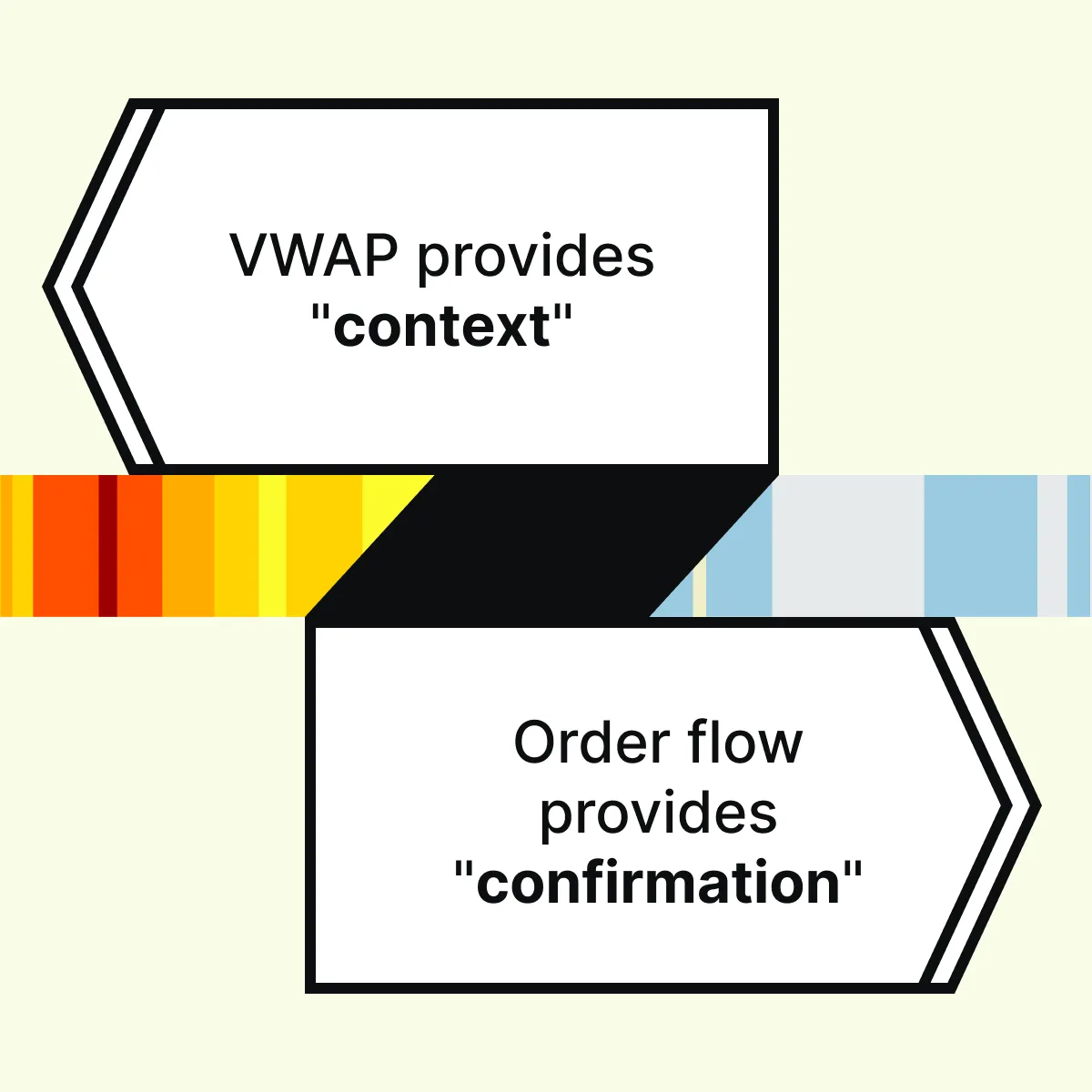

So, in this way, VWAP provides the context, but the order flow confirms the trade. Additionally, you must also observe in the Bookmap chart that:

- Risk is defined above the VWAP area, where the idea would be invalidated.

and

- Profit is taken at pre-identified liquidity below (not randomly).

Why This Trade Makes Sense Using VWAP

This example highlights a key idea in TWAP vs VWAP-

- VWAP shows where participation matters.

- Order flow shows how participants behave there.

By using VWAP, a trader can stay patient and avoid guessing. Also, they can align execution with real market activity.

In contrast, TWAP would offer no help here. That’s because TWAP does not react to volume, liquidity, or structure. It cannot show where sellers are active or where targets exist.

The Takeaway for Traders

The main lesson from this example is that:

For more real-market examples like this, you can explore additional insights from here – https://bookmap.com/insights

Conclusion

By now, it should be clear that although TWAP and VWAP are often mentioned together, but they are not interchangeable tools. In the discussion of TWAP vs VWAP, the key difference lies in “purpose”.

VWAP lets traders understand where the market agrees on value. It shows where real trading activity is concentrated and supports intraday bias. How to make it work best? You may combine it with order flow and liquidity analysis.

TWAP, on the other hand, allows institutions to execute large orders smoothly without drawing attention or disrupting the market. It follows time, not participation.

When used correctly, both tools are powerful in their own domain. When misused, they create false expectations. To make your interpretations more precise, you can even start using Bookmap. See how execution benchmarks interact with real liquidity → Compare Packages.

FAQ

1. What is the main difference between TWAP and VWAP?

The core difference in TWAP vs VWAP is what they measure. VWAP adjusts to where real trading volume happens. It shows where the market agrees on value. In contrast, a TWAP averages prices evenly and ignores market activity.

2. Which is more useful for day traders?

VWAP is more useful for day traders because it reacts to real-time:

- Trading activity,

- Liquidity, and

- Participation.

It allows traders to judge bias, balance, and whether the price is extended. All of these are critical for intraday decision-making.

3. Do institutions use both?

Yes, several institutions use both tools, but for different reasons. VWAP is mainly used as a “benchmark” to evaluate execution quality. On the other hand, TWAP is used to schedule large orders smoothly without moving the market.

4. How does Bookmap help with VWAP analysis?

Bookmap is an advanced real-time market analysis tool. It shows how liquidity and order flow behave around VWAP. Using Bookmap, traders can see whether trading activity increases, slows, or shifts. The benefit? Such tracking enables them to understand changes in acceptance, rejection, and participation near this key reference level.

Sign Up Now