See how markets respond after difficult quarters.

Compare plans to track positioning shifts and investor reactions as conditions change.

Education

May 12, 2026

SHARE

How Fund Investors Absorb a Tough Quarter: What Happens After Markets Disappoint

When headlines suggest that fund investors are absorbing a tough quarter, most retail traders interpret that phase as “inactivity” or “passive waiting.”

However, weak performance usually triggers a pre-determined response across large institutions. After such periods, managers reassess risk, carry out portfolio rebalancing after losses, meet redemption demands, and rotate exposure based on mandates.

These actions generate “investor flows” (after bad quarter phases) that are worth tracking.

Market moves around quarter-end and the start of a new period are mostly influenced by these adjustments rather than fresh news or sentiment. This is why price action can appear unusual, with steady trends, sudden reversals, or sector rotations.

This article explains how different funds adjust after weak performance and what drives those decisions. Also, retail fund investors will learn how these flows appear in markets and influence short-term price behavior.

First, What Counts as a Tough Quarter?

A tough quarter does not have a fixed definition. It depends on the:

- Fund’s strategy

- Benchmark, and

- Stated objectives

For example, a flat return may be viewed as “weak” if the broader market delivered strong gains. Usually, such a situation reflects poorly in mutual fund quarterly performance comparisons. In contrast, a 5% decline during a highly volatile phase may still be acceptable if peers or benchmarks fell more sharply.

Moreover, several factors can make a quarter difficult. These include:

In other cases, changes in market leadership (also known as “style rotation”) or unexpected macro events can negatively influence fund returns. At times, investor flows after bad quarter periods may also add pressure, as withdrawals force funds to adjust positions.

Therefore, a tough quarter is not judged by returns alone. It is evaluated against:

- Expectations

- Risk limits, and

- The fund’s mandate

That’s why fund investors surviving a tough quarter usually assess performance in “relative” terms and not in absolute terms.

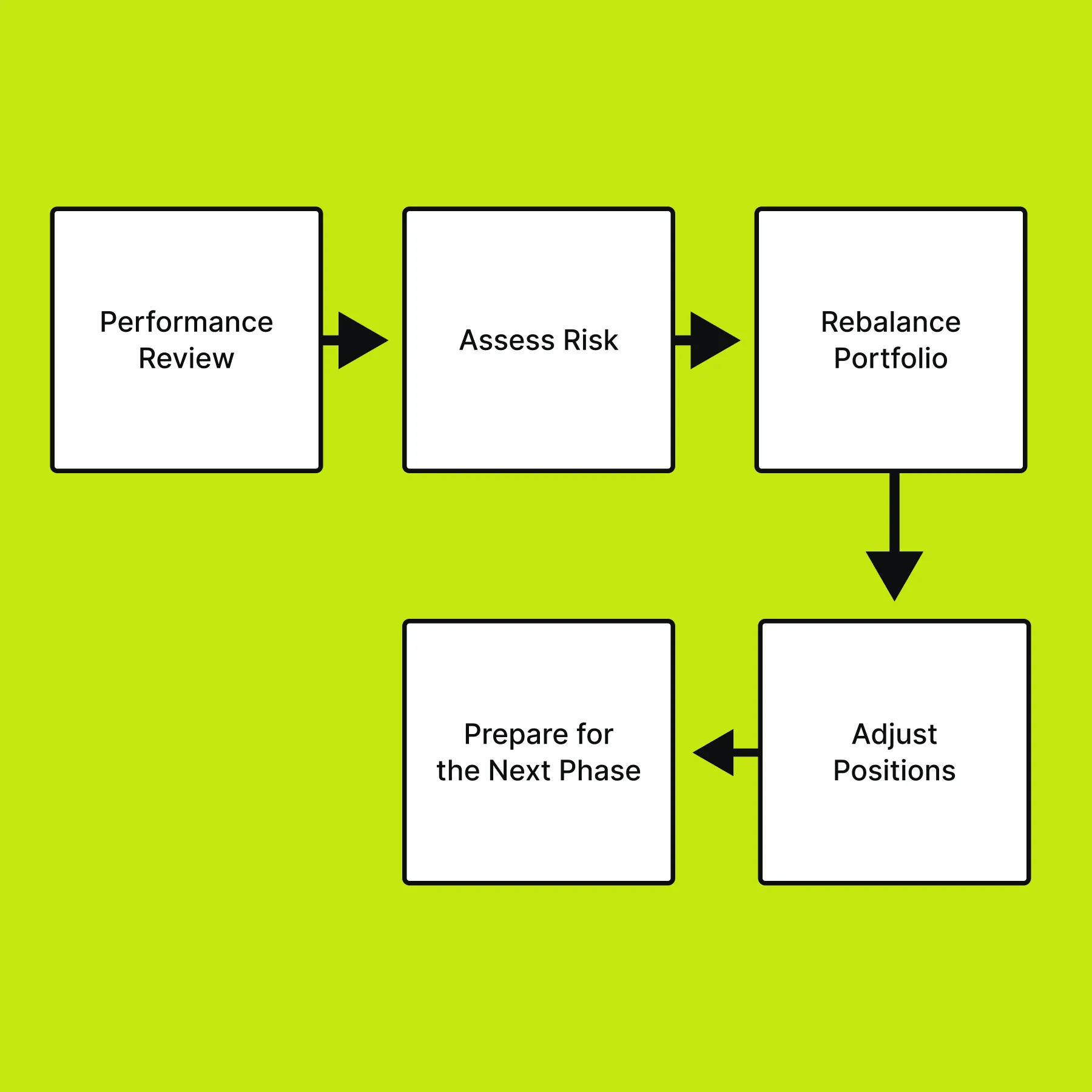

How Long-Only Funds Usually Respond

Traditional asset managers such as mutual funds, pension funds, and balanced portfolios may follow some pre-defined processes (or set of steps) after a weak period rather than reacting to short-term market moves. These steps are:

| Performance Review | Risk Assessment | Re-balancing After Losses | Portfolio Re-positioning |

|

|

|

|

As a result, their response is less about market sentiment and more about maintaining alignment with their mandate. For more clarity, let’s study an example,

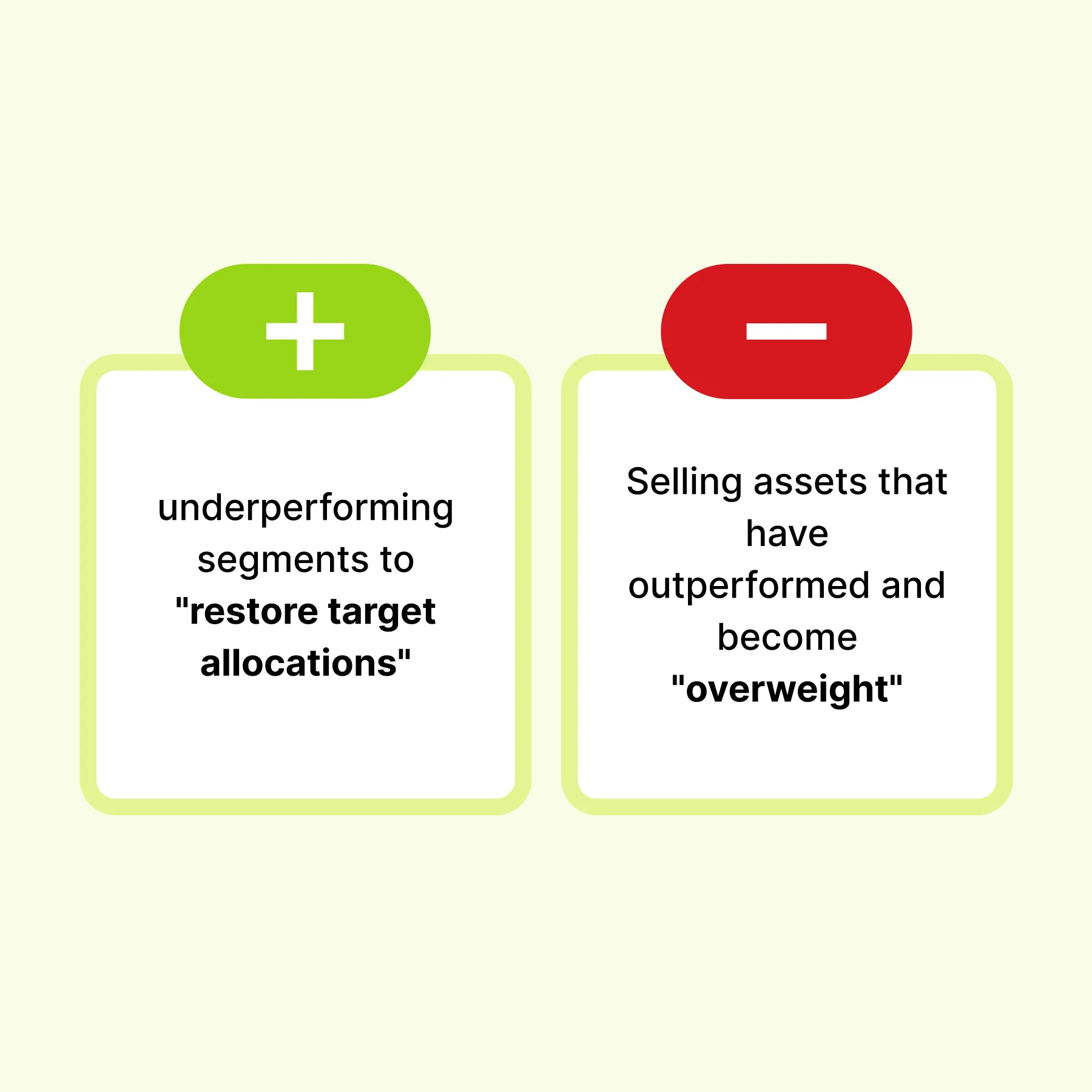

- Suppose equities decline while bonds rise.

- A balanced fund may buy equities and trim bond exposure to restore its target allocation.

- Consequently, such adjustments create noticeable month-end or quarter-end activity in markets.

However, investors must realize that this buying is usually “mechanical” in nature. It may not always reflect a positive outlook. Learn how large investors adjust after volatility shocks → Compare Packages

How Hedge Funds May React Differently

In contrast, hedge funds operate with greater flexibility but also face higher performance pressure. Therefore, hedge funds after losses usually adjust positions more actively. This may include:

- Reducing overall exposure

- Cutting underperforming themes

- Increasing hedges, or

- Rotating capital into areas showing stronger momentum.

At the same time, responses can vary across managers. Some may adopt a “defensive stance” to limit further drawdowns, while others take “selective risks” if markets appear mispriced. For example,

- A macro fund impacted by falling yields may reduce bond short positions and shift toward currencies or commodities.

- Similarly, a long/short equity fund may exit crowded trades and increase cash holdings.

As a result, hedge fund positioning can change more tactically. This is a primary reason why fund activities lead to sharper investor flows after bad quarter periods compared to traditional funds.

Redemptions Matter More Than Headlines Suggest

After a weak period, one of the less visible drivers is investor withdrawals. In such cases, investor flows after bad quarter phases can force funds to raise cash. As a result, managers may “sell holdings” even when their long-term view on those assets remains unchanged.

Now, this creates an important distinction. Market participants may interpret selling as a negative signal, while in reality, it may reflect liquidity needs rather than conviction. Therefore, pressure from redemptions can influence future positioning (which is one of the most overlooked parts of how funds respond to volatility).

Why Quarter-End Rebalancing Can Move Markets

At the same time, quarter-end periods may bring “coordinated activity” across funds. Since many portfolios adjust positions around similar dates, portfolio rebalancing after losses and gains can lead to noticeable price movements. This process may involve:

In addition, funds may adjust currency hedges, use futures for exposure changes, or align positions with index requirements. For example,

- Suppose equities recover late in the quarter after earlier declines.

- Some funds may still sell into strength to rebalance.

- Conversely, if markets fall sharply near quarter-end, balanced mandates may require fresh buying.

As a result, these mechanical adjustments may influence mutual fund quarterly performance trends. Such trends are closely tracked during the final days of a reporting period. Understand how institutional flows can move markets → Compare Packages

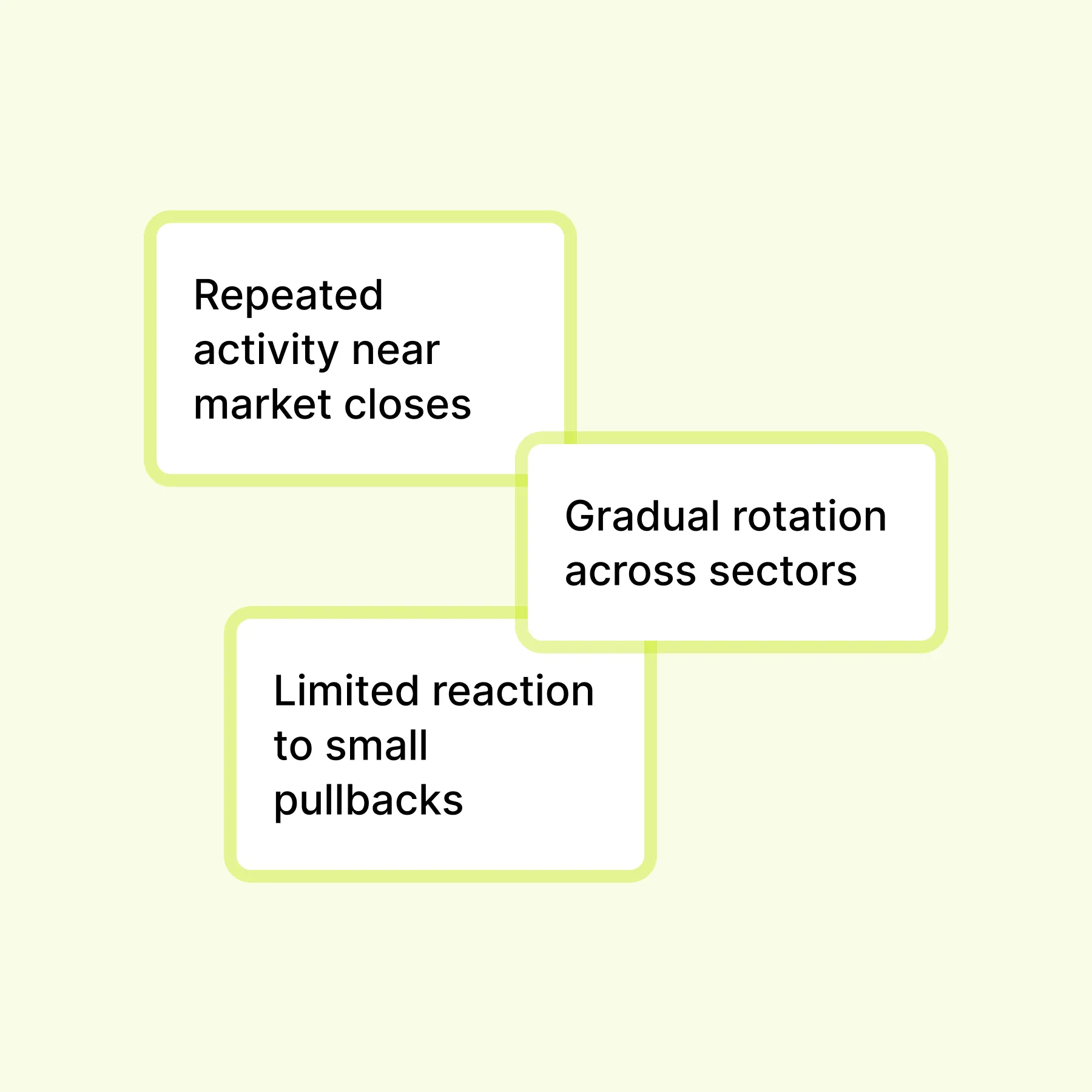

What Traders May Notice on the Tape

Mostly, large fund activity appears different from short-term speculative trades. Instead of sharp and sudden moves, institutional adjustments may show as steady buying or selling over extended periods. This can include:

As a result, markets may move in a slow and consistent manner. For example,

- An index may rise throughout the afternoon session.

- There could be an absence of any sharp spikes.

- This may happen due to the execution of large buy programs in parts.

In such cases, price action reflects size rather than urgency. Therefore, not every slow move signals weakness. Instead, it may indicate “underlying investor flows” after bad quarter adjustments or asset allocation changes.

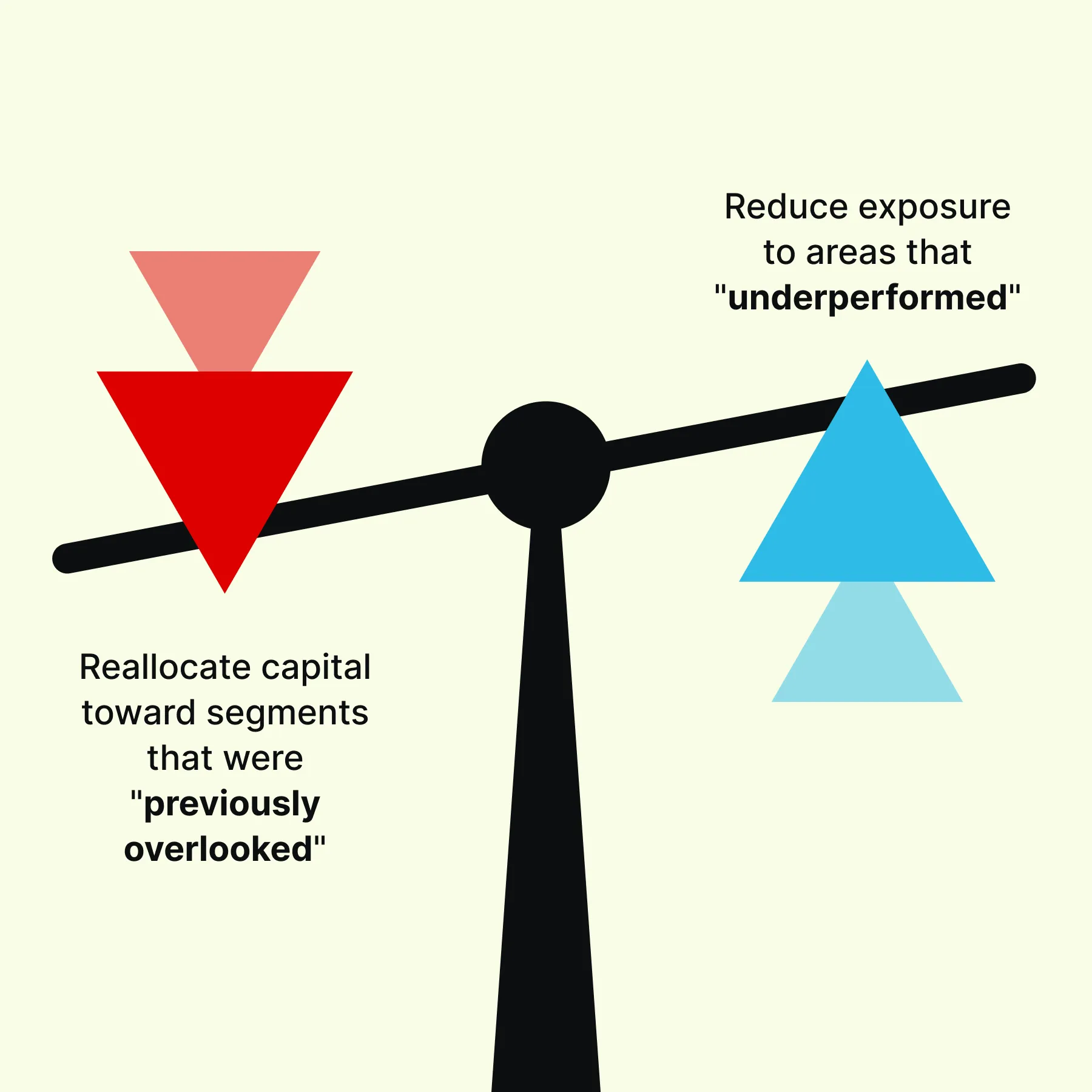

Tough Quarters Often Change What Works Next

At the same time, weak performance periods could lead to a reassessment of strategy. This is where mutual fund quarterly performance plays an important role in influencing future positioning. To reposition, managers may:

To perform such repositioning, the fund managers may indulge in several “rotations,” such as:

- From Growth to Value

- Domestic markets to international exposure

- Large-cap dominance to broader participation, or

- Equities toward bonds

In addition, speculative themes may give way to more defensive positioning. Therefore, a tough quarter fund investor phase does more than only reflect past outcomes. It also influences what comes next. In most cases, portfolio rebalancing after losses and allocation changes sets the foundation for new trends in the following quarter.

What Retail Traders Can Learn From This

After a weak period, retail activity may reflect emotional reactions, which can lead to rushed decisions. In contrast, institutional behavior shows a pre-determined response to volatility. This usually involves:

- Reviewing overall exposure

- Adjusting risk levels, and

- Cutting positions that no longer align with current conditions.

As a result, the emphasis shifts from short-term recovery to stability and flexibility. This is similar to portfolio rebalancing after losses, where the goal is to realign with the strategy rather than chase immediate gains. At the same time, capital is preserved to allow participation in future opportunities.

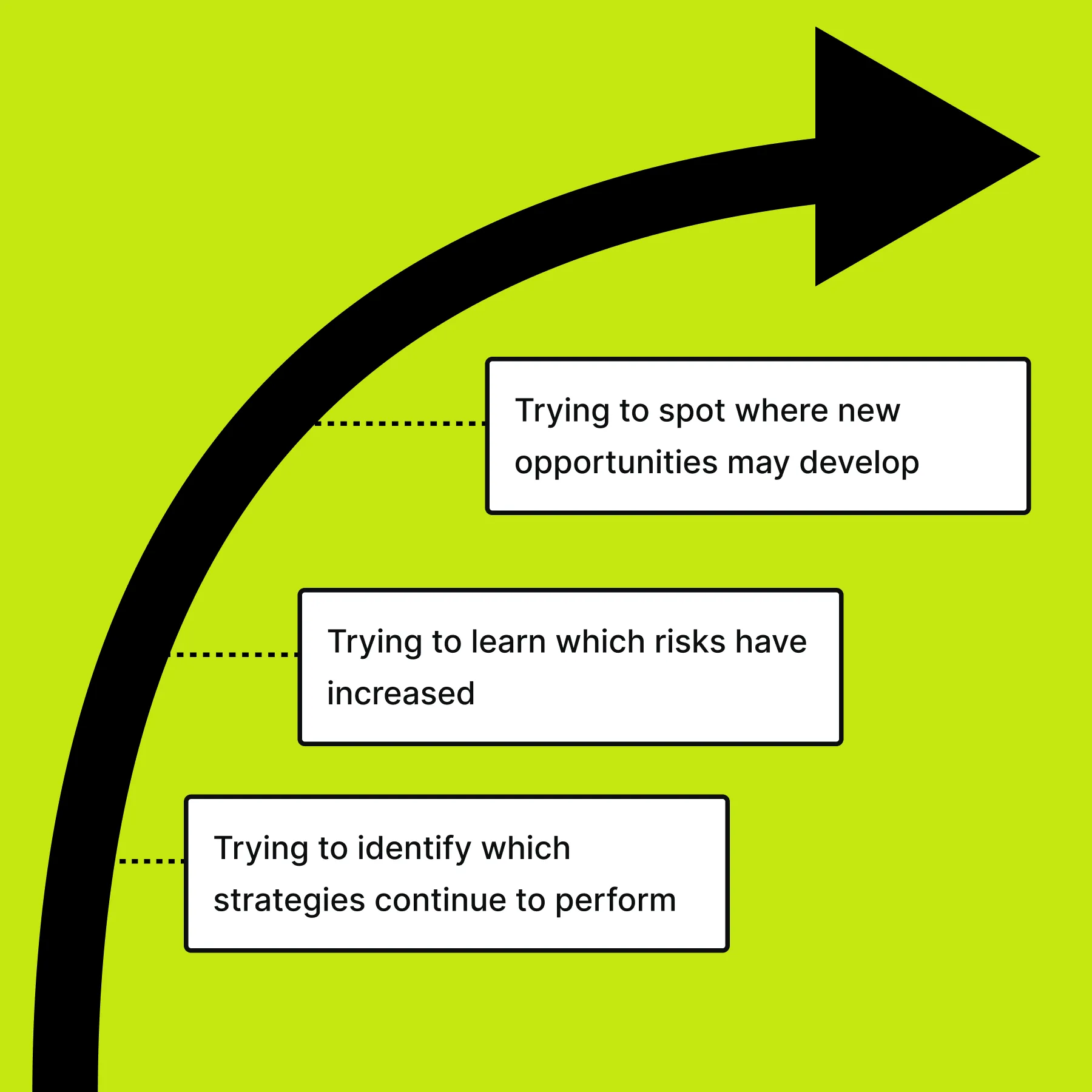

Therefore, instead of reacting to recent losses alone, retail market participants may try to reassess what has changed. This includes:

Such an approach reflects the broader discipline seen during tough quarter fund investor phases, where decisions are guided by process rather than urgency. See how rebalancing pressure appears in real time → Compare Packages

Conclusion

When markets go through a weak phase, fund investors surviving a tough quarter try to actively adjust their portfolios. Usually, this includes portfolio rebalancing after losses, raising cash to meet redemptions, or rotating into new themes that better match current conditions.

At the same time, investor flows after bad quarter periods can influence how and when these changes happen, which often creates market moves that appear sudden but are driven by planned actions. As a result, price behavior near quarter-end or shortly after can reflect these adjustments rather than fresh sentiment.

Therefore, tracking mutual fund quarterly performance and positioning changes can explain why leadership shifts and trends evolve after volatility phases. Learn how large investors adjust after volatility shocks → Compare Packages

FAQs

1. What does it mean when funds absorb a tough quarter?

It means funds do not stay idle after weak performance. They review results, check risks, and adjust positions. This may involve:

- Portfolio rebalancing after losses

- Cutting weak trades, or

- Preparing for changes in investor flows after bad quarter periods

The goal is to stay aligned with their mandate and not to react emotionally to short-term losses.

2. Do funds always sell after a bad quarter?

No, selling is not the only outcome. Some funds may reduce exposure, while others may buy to restore target allocations. This depends on strategy and positioning. In many cases, funds follow a fixed process during volatile periods. Usually, their decisions come from rules and portfolio needs, not from a negative view of the market.

3. Why do markets move strangely at quarter-end?

Quarter-end brings planned adjustments from large funds. At this time, funds are adjusting after their quarterly results and bringing their portfolios back in line with their investment rules. The actions they may take are:

- Rebalancing

- Hedging, and

- Asset allocation changes

As a result, price moves look unusual as they are influenced by size and timing (and not new information).

4. Can traders benefit from understanding fund flows?

Yes, and that’s because not all price movements are a result of market sentiment. Some moves are influenced by rebalancing or redemption needs. By recognizing investor flows after bad quarter phases, investors may spot slow trends or sudden shifts. This provides better context for price action and separates mechanical moves from genuine directional intent.

Sign Up Now