See how market makers actually manage liquidity and risk.

Compare plans to follow inventory shifts, absorption, and price reactions as they develop.

Education

May 28, 2026

SHARE

How Do Market Makers Actually Hunt? What They’re Really Doing (And What Traders Misunderstand)

Retail traders describe sharp moves with phrases like “the market makers hunted my stop” or “price was pushed there on purpose.” However, this view oversimplifies how modern markets function.

In reality, what market makers actually do is far more mechanical. Their role revolves around providing liquidity, managing inventory, reacting to incoming orders, capturing the bid–ask spread, and controlling risk during sudden moves. This information changes the perspective on how market makers hunt stops. What appears as “deliberate targeting” is mostly the result of price moving toward areas where orders are concentrated.

Read this article to better understand market maker strategy and how they operate today. Also, learn how to interpret price behavior in terms of liquidity, incentives, and participation rather than based on assumptions.

First, What a Market Maker Is Actually Paid to Do

A market maker’s primary job is to quote both sides of the market. They continuously post bids (buy prices) and offers (sell prices) to maintain a highly liquid trading environment. In return, their compensation comes from “repeatable edges” rather than large directional bets.

Usually, these edges are:

- Spread capture, where market makers earn the difference between the bid and offer,

- Exchange rebates or incentives in certain venues,

- Hedging advantages when offsetting risk across instruments,

- Flow internalization when the opportunity is available in some markets,

- High-frequency turnover with small margins.

Therefore, the idea that market makers mainly profit by moving prices is incomplete.

A more accurate view of what market makers actually do is that they facilitate trades and collect small gains many times over.

Their behavior can be understood better through an example related to futures market makers trading, such as the ES (S&P 500 futures), where the spread is usually “one tick”:

- Assume that a market maker repeatedly buys at the bid and sells at the offer.

- They manage risk and accumulate these small gains through volume.

- As a result, market makers make money without requiring large price manipulation.

What “Hunting” Usually Means in Practice

In the markets, there is a common phrase: “market makers hunt stops.” Such a “hunting” usually happens when:

This behavior does occur; however, the cause is usually structural rather than intentional targeting of individuals. Realize that markets usually move toward areas where orders are concentrated.

In other words, price seeks liquidity. As a result, liquidity clusters around predictable levels, such as:

- Prior highs and lows,

- Equal highs or equal lows,

- Breakout zones,

- Obvious support or resistance, and

- Trendline invalidation points.

Since many traders place stop-loss orders at these levels, large pools of executable orders accumulate there. Therefore, when prices move into these zones, it may appear as if market makers hunt stops. However, this move is a result of “search for liquidity” rather than a targeted action.

Furthermore, it is worth mentioning that this process may benefit multiple participants, for example,

- Market makers can manage inventory through available orders, and

- Larger players can execute sizable trades.

Also, triggered stops can create momentum, and the market can establish a new balance after liquidity is absorbed. Thus, what appears to be stop hunting is usually the natural outcome of how markets organize around order concentration.

Understand the difference between stop hunts and normal market mechanics → Compare Packages

In Highly Liquid Markets Like the S&P, The Job Is Often Simpler Than Traders Think

Many traders assume that instruments like ES or SPX futures can be traded only through constant, complex manipulation. However, in highly liquid markets, such trading is more mechanical and repeatable. The following points reveal what market makers actually do in such markets:

- They may quote prices around a “fair value.”

- Adjust quotes based on related markets like ETFs or other indices,

- Widen or tighten spreads during volatility shifts,

- Manage inventory based on incoming buy and sell flow, and

- Hedge exposure when positions become unbalanced.

Realize that, since ES trades at very high volume, competition among participants is intense.

Consequently, no single player can influence the price for long periods. Instead, price movements are influenced by many competing flows rather than a single dominant force.

An example of this dynamic is provided below:

- Assume that strong economic data triggers heavy buying.

- A market maker initially sells at the offer.

- However, continued buying creates a short position.

- Because of this, risk exposure increases, and the market maker responds by:

- Buying back positions at higher prices,

- Hedging in related markets,

- Temporarily widening spreads, and

- Repricing quotes upward.

This sequence may appear erratic on a chart. However, such a market scenario reflects “inventory adjustment” under pressure rather than deliberate price control.

How Algos Actually Influence Short-Term Price

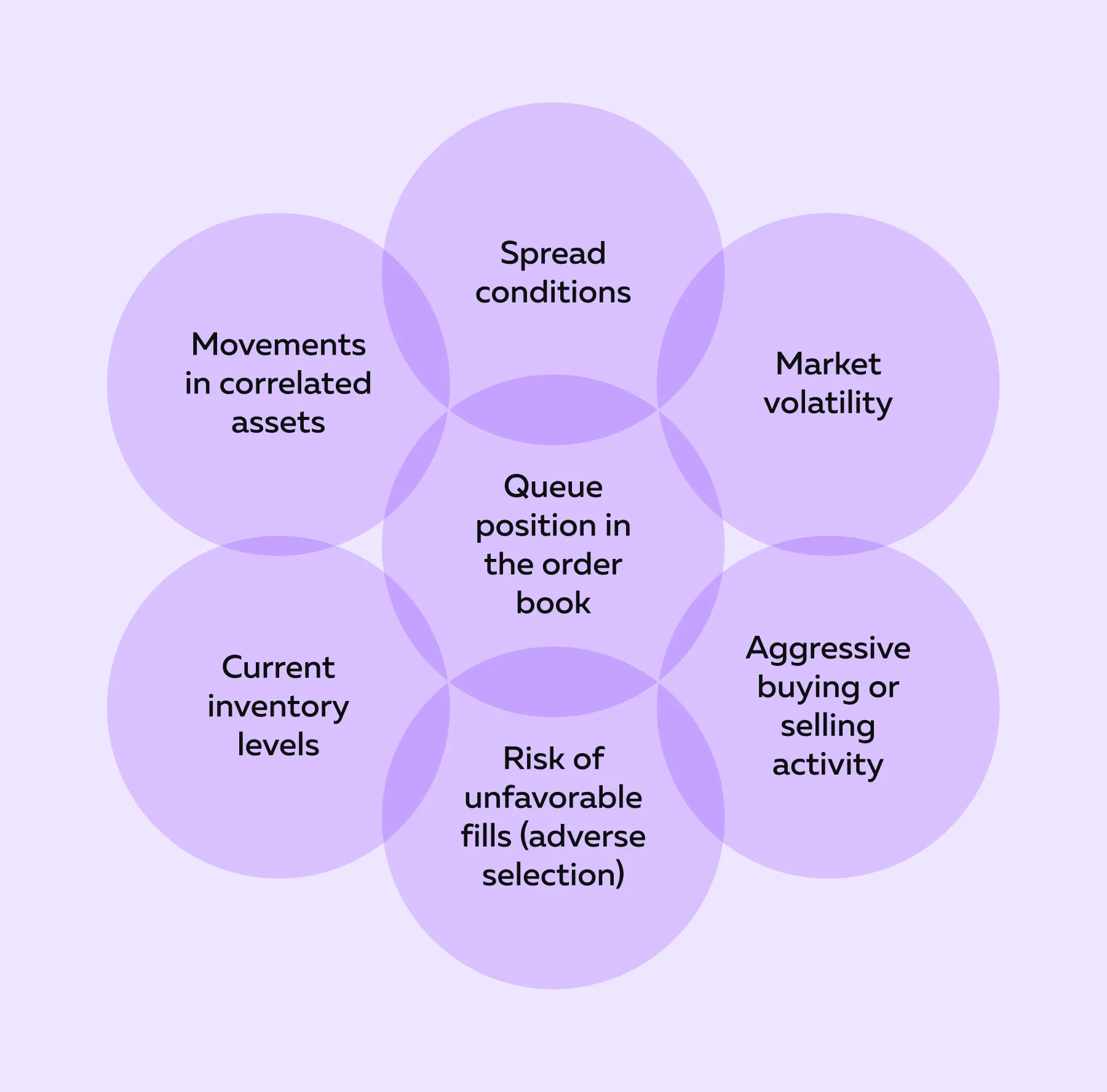

Algorithmic trading is often viewed as highly complex or predictive. However, in reality, many market-making systems operate on “rule-based” responses. These systems react to several real-time inputs, such as:

Therefore, these systems are not designed around predicting individual stop levels.

Instead, they adjust behavior based on shifting probabilities and order flow. This dynamic is demonstrated in the following example scenario:

- Aggressive buyers repeatedly lift offers.

- Related markets also move upward.

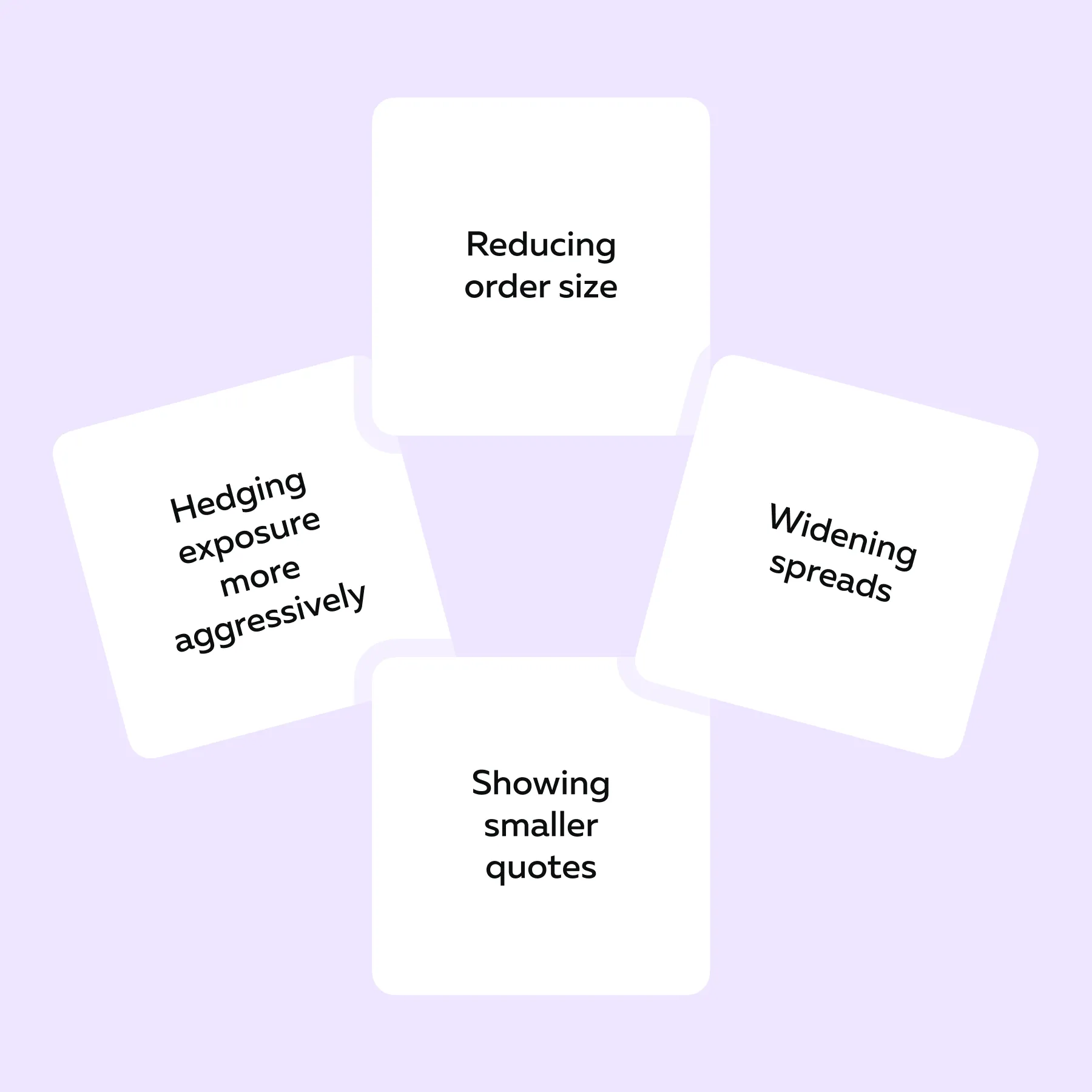

- The algorithm reacts by:

- Removing existing sell orders,

- Posting new offers at higher prices,

- Reducing visible order size, and

- Supporting bids at slightly higher levels.

- This creates a sharp upward price move.

To many observers, this may resemble how market makers hunt stops. However, the behavior is better described as dynamic repricing based on demand.

When Market Makers Become Defensive

One of the most misunderstood situations in markets occurs when liquidity suddenly drops.

At first glance, this is often labeled as “manipulation”. However, a more accurate explanation could be that:

- Risk has increased, and

- Liquidity providers step back.

This behavior usually appears during uncertain conditions, such as:

- Major news releases,

- Events like CPI, FOMC, or NFP,

- Unexpected geopolitical developments,

- Sudden momentum bursts, and

- Thin overnight sessions.

As uncertainty rises, quoting tight bid–ask spreads becomes risky. In response, what market makers actually do changes from active participation to risk control. Market makers usually manage risk in the following manner:

Consequently, the price can move more sharply than usual. In fact, the absence of liquidity can move the price more than active trading.

How Traders Misread Stop Sweeps

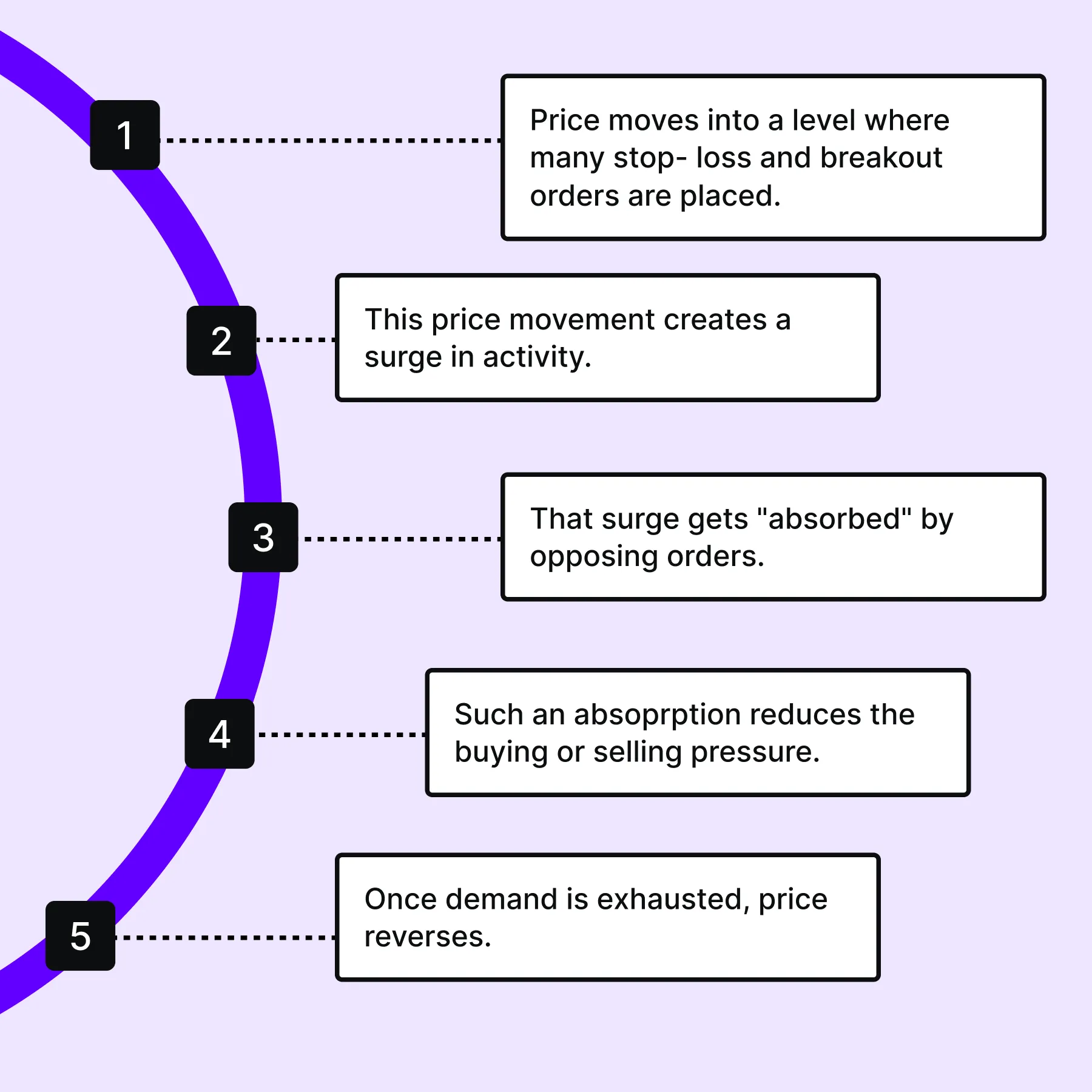

A common market pattern occurs when the price moves slightly beyond a known level and then reverses. Usually, this is described as how market makers hunt stops. A common sequence looks like this:

- Price trades above a prior high by a small margin,

- Stop-loss orders and breakout entries are triggered, and

- Price then reverses direction.

This behavior leads to a common belief: market makers hunt stops. However, a more complete explanation is based on liquidity and order flow. Note that obvious highs and lows contain clusters of stop orders. These areas also attract breakout traders. Due to this, liquidity builds around these levels, particularly when the price reaches them.

The following events may occur next:

- Aggressive buyers enter the market, and

- Passive sellers absorb that demand.

Consequently, buying pressure reduces, and the price rotates lower. Traders must realize that a single participant does not drive this sequence. Instead, it involves multiple market participants operating at the same time, such as:

| Participant | What They Are Doing | Why It Is Important to Price Movement |

| Market Makers | Managing inventory by buying and selling around the current price | Their activity provides liquidity, but they also adjust positions, which can push the price in the short term |

| Institutional Participants | Executing large buy or sell orders over time | Their size creates real demand or supply, which can drive sustained price movement. |

| Momentum Traders | Entering trades when the price breaks key levels | Their entries add pressure toward the breakout, which may extend the current price move. |

| Trapped Traders | Exiting losing positions after price moves against them | Their exits add fuel to the opposite side, which usually accelerates reversals |

Therefore, the price movement in such trading scenarios is influenced by how markets process concentrated orders. Initially, what appears as “deliberate stop hunting” is actually the result of liquidity being accessed and then exhausted.

What Retail Traders Should Learn Instead of Blaming Market Makers

While conducting market analysis, traders may shift from “personality-based” to “incentive-based” thinking. Rather than asking who is controlling the price, stronger observations come from questions like:

- Where is liquidity concentrated?

- Which participants are likely trapped at current levels?

- Is the price accepted beyond a key level or rejected?

- Is visible liquidity being held or pulled?

- Does momentum show continuation or a brief sweep?

- Would a liquidity provider stay active here or step back?

These questions align with what market makers actually do: managing liquidity and order flow risk. As a result, analysis becomes grounded in structure rather than assumption. Always remember that such a perspective improves trade execution, while blame offers no analytical value. Read order flow instead of guessing who is in control → Compare Plans

The Truth About Market Makers and Directional Moves

Another common belief is that market makers create large trends. However, their incentives often suggest the opposite. Note that market makers usually prefer balanced conditions because:

- Two-way movement allows repeated spread capture,

- Stable spreads reduce risk exposure, and

- Orderly markets support consistent participation.

If we talk about how market makers make money, their returns are usually built through steady activity rather than large directional bets. Traders must realize that when strong trends develop, inventory risk increases. A one-sided move in such situations can leave positions exposed and harder to manage.

Due to this, in futures market-making, trends are driven by broader market demand or institutional flows. Market makers then adjust to that movement rather than initiate it. Thus, price direction is a response to external pressure (and not a controlled outcome).

Conclusion

The idea of how market makers hunt stops comes from how the price behaves near obvious levels.

However, in most cases, the process is not about targeting any single trader. Instead, what market makers actually do revolves around seeking liquidity, managing inventory, and capturing small spreads.

Furthermore, in highly liquid markets like the S&P, price moves are influenced by competition, order flow, and constant repricing. Because of this, what may look like manipulation is usually a normal reaction to changing conditions.

This dynamic also explains how market makers make money: through repeated small edges rather than large directional moves. Thus, trading progress may come from reading liquidity and participation rather than assuming intent. See how liquidity providers actually behave in real time → Compare Packages

FAQs

1. Do market makers hunt individual retail stops?

In most cases, the idea behind how market makers hunt stops is misunderstood. Price usually moves toward areas where many stop orders are placed, such as highs or lows. This behavior occurs because those zones contain liquidity. Due to this, moves are driven by order concentration rather than targeting individual traders.

2. How do market makers make money?

Most of their gains may come from repeated trading edges, such as:

- Earning from the difference between buying and selling prices (spread),

- Managing risk through hedging, and

- Trading frequently.

Instead of earning from major price moves, they build profits over many transactions with controlled exposure.

3. Are market-making algos highly advanced AI systems?

Some systems are advanced, but most follow pre-defined trading rules. Such algos usually react to factors like:

- Price movement,

- Order flow, and

- Inventory levels.

They adjust quotes based on market conditions rather than predicting exact outcomes or targeting specific traders.

4. Why does the price jump when news hits?

After the release of any major news, market uncertainty increases. In such moments, market makers actually reduce participation by widening spreads or pulling orders, thereby reducing available liquidity. As a result, even normal buying or selling pressure can move the price sharply, leading to sudden market jumps.

Sign Up Now